.png)

Executive Summary: Bitcoin in Q1 2026

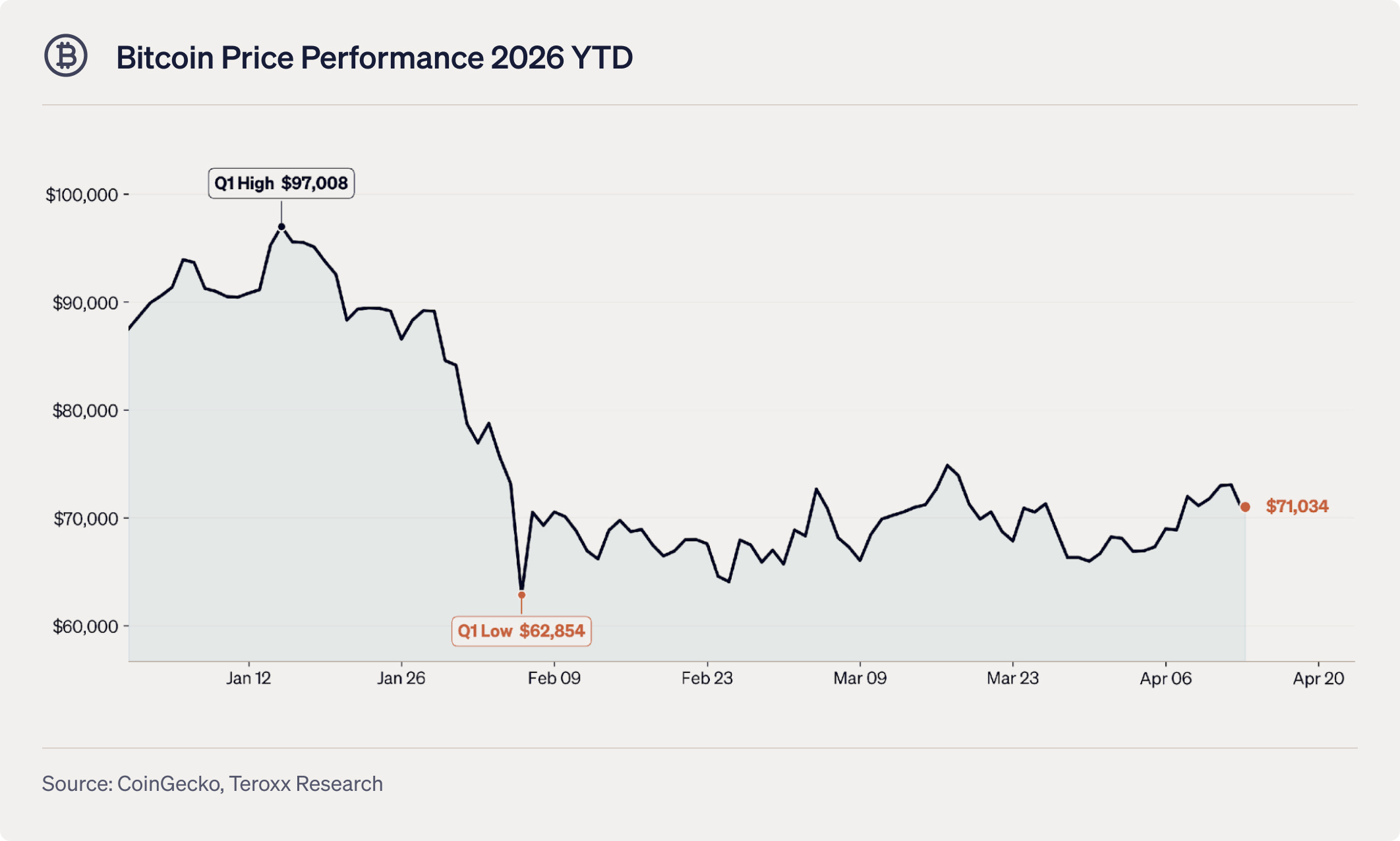

Q1 2026 delivered a punishing -23.8% return, extending the correction from Q4 2025 and marking two consecutive negative quarters — the worst sequential drawdown since Q2–Q3 2022. After opening at $87,520, Bitcoin briefly rallied to a Q1 high of $97,008 (January 15) before declining to a low of $62,854 (February 6) — a 35.2% peak-to-trough drawdown. The quarter closed at $66,699.

The quarter was defined by an unprecedented convergence of headwinds: escalating US trade policy uncertainty, the outbreak of the US-Israel-Iran conflict (February 28) and closure of the Strait of Hormuz, persistent inflation delaying rate cuts, and cascading liquidations. Yet against this turbulence, Q1 also delivered some of the most significant structural developments in Bitcoin’s history — including the US Strategic Bitcoin Reserve executive order (March 6) and the SEC-CFTC joint classification of 16 cryptocurrencies as digital commodities (March 17).

As of April 13, 2026, Bitcoin has recovered to ~$70,659 — up approximately 5.9% from the March 31 close — bolstered by the landmark launch of Morgan Stanley’s spot Bitcoin ETF (MBST) on April 8.

-2.jpg?width=2124&height=1180&name=Chart%20Base%20(1)-2.jpg)

The broader crypto market suffered even more severely. Ethereum declined approximately -30% in Q1, pushing the ETH/ BTC ratio toward multi-year lows. Bitcoin dominance rose to 56.8%, reflecting relative resilience as altcoins bore the brunt of liquidations.[1]

-1.jpg?width=2124&height=1104&name=Chart%20Base%20(2)-1.jpg)

Q1 2026 Event Timeline

The quarter featured an extraordinary density of macro, geopolitical, and regulatory catalysts.

The Iran Conflict and Energy Shock

The single most impactful event of Q1 was the US-Israel joint military strike on Iran on February 28, which included the killing of Iran’s supreme leader. Iran retaliated with attacks on US bases, Israeli territory, and Gulf states, and the IRGC closed the Strait of Hormuz — through which 20% of global oil transits.[4]

The IEA characterized this as the “largest supply disruption in the history of the global oil market.” Brent crude surged from ~$73/bbl to $126/bbl at its March 8 peak. Bitcoin dropped from ~$70,000 to below $63,000 within hours, confirming that during acute geopolitical stress, Bitcoin still trades as a risk asset — in stark contrast to gold, which spiked to an all-time high of $5,294/oz on March 2.

Trade Policy Whipsaw

On February 20, a US court ruled many of Trump’s tariffs illegal — but within hours, the administration imposed new tariffs starting at 10%. The April 2 “Liberation Day” reciprocal tariffs added a baseline 10% duty on all imports targeting ~60 nations, creating persistent uncertainty across risk assets.[5]

Fed Policy Paralysis

The Fed remains caught between sticky inflation (~2.7% CPI) and geopolitical risk. Markets now price only 1–2 rate cuts in 2026, down from 4+ expected at the start of the year. The balance sheet has stabilized at ~$6.4–6.5T following QT’s end in December 2025